Dethrone: From Quantitative Easing to Digital Currencies - What's Next for the Dollar's Status Quo? (Part 1)

In the long run we are all dead.

- John Maynard Keynes

QE and Inflation Theory (Part 1)

Oversupply Always Leads to Devaluation | June 2015

This fundamental economic principle is well-known to most of us. When there's an oil glut, prices plummet. When a country has an excess of working-age population, wages tend to be suppressed.

For the past 3-4 years, governments worldwide have been printing money under the banner of Quantitative Easing (QE), following the advice of Keynesian economists. This has led to a global excess of money supply. Austrian school economists, who oppose government intervention in the economy, were confident that this would lead to a significant devaluation of currency or even hyperinflation. However, the reality has diverged considerably from their predictions.

It's not that Keynesian economists were right and Austrian economists were wrong. In truth, both schools of thought missed the mark.

Some argue we're in a period of deflation, while others claim we're experiencing inflation. Surprisingly, both can be correct. Deflation and inflation are not mutually exclusive; they can occur simultaneously.

The current global economic situation is characterized by deflation (a significant decrease in money circulation) coupled with rising prices (inflation).

Traditionally, it was believed that during economic downturns, people have less money, goods don't sell, and prices eventually drop to a point where people can afford to buy again. This meant that as money became scarcer, its value increased relative to goods, allowing a smaller amount of money to purchase more. This is the deflation that people feared.

However, economic theories have evolved significantly in the modern world.

Despite the massive money printing through government QE programs, this money hasn't reached the hands of the general public. Consequently, people don't feel that money is easily obtainable, even though the money supply has increased. We don't sense that money has become cheaper.

As people struggle to make ends meet, feeling that money is increasingly difficult to come by regardless of how much the government prints, anything perceived as scarce tends to be hoarded.

Naturally, most people hoard money for future use, making it even scarcer. This situation reflects the severe deflationary trend occurring globally.

However, this modern deflation doesn't lead to price reductions as traditional economic theory would suggest.

In today's deflationary environment, sellers can't lower prices due to rising production costs. When prices increase during a period of deflation, it's traditionally called stagflation (a combination of stagnation and inflation).

But the stagflation of 2015 differs significantly from that of 1983.

In 1983, oil prices skyrocketed due to the Iranian Revolution, inevitably increasing production costs worldwide. In contrast, in 2015, oil prices dropped by 50%, yet our cost of living didn't decrease at all.

The root cause lies in the failure of government fiscal management. Central banks have been printing money excessively, increasing government costs without solving economic problems or generating productivity. The result will be an ever-increasing debt burden for governments, especially in money-printing superpowers like the US, the UK, Japan, and most recently, the Eurozone.

These rising government costs are what's driving up the prices of almost everything in the world.

However, we're still far from hyperinflation. Contrary to popular belief, hyperinflation isn't caused by unlimited money printing by governments. It actually stems from a collapse in confidence in the government. Before that point, we'll likely experience the most severe money shortage in history. (The clearest evidence is that US has been printing money for four years, yet the dollar has been consistently strengthening, while commodity prices, including gold, show no signs of bullishness or hyperinflation trends.)

If the money governments are printing isn't reaching the public, where is this vast amount of money in the global economy? The key focus of economic theory in today's world should be on capital flow rather than traditional supply and demand models.

To fully understand this new economic puzzle, we need to delve into topics like hyperinflation, capital flow, deflation, interest rate policies, and exchange rates. I'll continue to write about these subjects in future posts.

QE and Inflation Theory (Part 2)

Hyperinflation | June 2015

What is the definition of “Hyperinflation” ?

Hyperinflation is a situation where "money devalues so much that no one wants it." When you receive money, you rush to convert it into any asset as quickly as possible.

Confidence in the state collapses, and no one wants money anymore. As a result, prices of goods skyrocket rapidly. An egg that used to sell for 5 baht might cost 1 million, and still, no one would want to sell it.

A millionaire with a million baht in the bank would suddenly find their wealth reduced to the value of a single meal. Everyone would rush to abandon cash, as no one believes that money will have any exchange value anymore. They would hoard any assets that can be exchanged for basic necessities.

For those who think this scenario is impossible, I encourage you to study world history. Hyperinflation has occurred countless times on this planet, including:

- Weimar Republic (Germany) after World War I: Inflation rate of 21% per day

- Yugoslavia during its breakup in 1994: Inflation rate of 65% per day

- Zimbabwe during money printing in 2008: Inflation rate of 98% per day

- Hungary after World War II: Inflation rate of 207% per day

This information is readily available on the internet.

The inflation theory suggests that the Quantitative Easing (QE) by world powers would lead countries like the US to experience hyperinflation, and the dollar would eventually collapse.

I used to believe this a few years ago, but now I admit I was wrong.

I want to share a perspective as an alternative source of information so that we can see a clearer picture of the "New Economics" where old theories from textbooks no longer apply.

Zimbabwe printed money heavily until the country collapsed.

So why, when the US is following a similar path, are the results so different?

First, we need to define "hyperinflation" clearly.

For me, it's the "complete" loss of confidence in a particular currency. It's not just severe inflation like what occurred in the world during the 1980s (when inflation might reach 20% or 100%). As long as citizens still have confidence in the state and want to hold the currency, it's not hyperinflation.

Hyperinflation is when most people are willing to abandon money for other assets without hesitation. State confidence collapses. At that point, all asset prices rise at an accelerating rate, not because their value has increased, but because the value of money has decreased to zero.

After a hyperinflation crisis, a country's financial system is always reformed. It's the point where the old currency permanently collapses, and a new currency is created to replace it. For example, after the French Revolutionary War that changed the country's governance foundation in 1641, hyperinflation occurred, causing the old currency, Livre tournois, to collapse. The new French government introduced the Franc in 1795, which continued for hundreds of years until it was replaced by the Euro in 1999.

In economic terms, hyperinflation is when the velocity of money increases to its extreme after money printing.

But let's look at the US dollar. The velocity of money in the US today is at its lowest point in 100 years of history. The dollar in 2015 changes hands even more slowly than during the Great Depression of 1929.

It's the opposite! The US implements unlimited QE, but people still hold onto dollars.

The main reasons why the US is not close to a hyperinflation scenario are:

- Everyone still holds dollars - Are you familiar with the petrodollar? It's an agreement between the US and OPEC countries that forces all nations to trade oil exclusively in US dollars. Any country that breaks rank faces potential war. As long as oil remains the world's primary energy source and trade continues in dollars, hyperinflation or abandonment of the dollar is unlikely to occur.

- The bond market remains intact - If you were a US creditor, would you allow the US to go bankrupt? The dollars you lent to the US would vanish instantly in the event of hyperinflation. Third-world countries like Zimbabwe can easily experience hyperinflation because their governments print money to pay off debts, leaving no creditors with an interest in maintaining the currency's value. But the US (for now) is different. Creditors pressure the debtor, demanding they find ways to increase revenue to repay debts - raise taxes, generate income, squeeze money from citizens, extract funds from businesses, whatever it takes.

In the near future, the European debt crisis is likely to intensify. The euro will be severely shaken by the worsening public debt crisis. Capital flow from Europe and around the world will flood into the US dollar. The dollar will strengthen dramatically during the European crisis. (I don't think the Chinese yuan will inspire investor confidence in the near term. The Chinese dragon will certainly rise to the top, but it still needs time to accumulate prestige.)

As Europe collapses, capital markets in other countries will suffer as capital flows out to hold dollars. Gold prices will drop sharply, potentially falling below $1,000 per ounce. (I still believe in gold, but at this time, I think it's highly likely that gold will fall heavily during the deflation period before rebounding after the US economic crisis hits.) Debtors in third-world countries will experience severe deflation due to rapidly increasing debt burdens from dollar-denominated loans.

2024 Update

About 6 months after I wrote this article, gold tested around $1,000 but didn't fall below $1,000 as I predicted. In the years that followed, gold did enter an uptrend as I thought, but it came with the Covid-19 pandemic, not from the US economic crisis as I had anticipated.

Our world is not at risk of a hyperinflation crisis as feared. On the contrary, we are about to face an Extreme Deflation crisis or severe money shortage in the global economic system. At some point, deflation will reach its peak, and then the pendulum will swing back in the other direction.

Years later, after capital flows into the US, the US will face problems greater than what collapsed Europe experienced, likely the worst economic crisis in 250 years of history.

A new global financial system will emerge within the coming decade, but whether it will be before or after the US crisis, I cannot say. There are still many variables in the economic system, including China and Russia, which we haven't discussed.

But all the superpowers that will face crises after this will be due to "Sovereign Debt Crises," pure and simple, whether it's Europe or the US. When I have time, I'll continue to discuss the main issues of the public debt crisis, which originates from the bond market and interest rates, followed by the new global financial system that is likely to emerge from the worldwide debt crisis.

QE and Inflation Theory (Part 3)

Why Does the US Need to Raise Interest Rates? | July 2015

"Money" in today's global economic system has several anomalies:

- The amount of money in the world has increased significantly due to QE, but the "true role of money" in this era is not being used for buying and selling goods (Medium of Exchange). Instead, it's used as a tool for speculation.

- Therefore, when we try to predict the future by adhering to the "context of money" from the past, the results are inaccurate. The printed money doesn't flow into the world of commerce but into another world we're unfamiliar with. (Money is printed, but there's no inflation, and the economy doesn't recover.)

- Moreover, in this era, money doesn't just circulate within a single country as it did in the past. It flows back and forth in the global economic system from one place to another in a single click, following higher returns. This has become a crucial factor driving capital markets in the globalized world.

For instance, whether stocks rise or fall in the short term these days has little to do with a country's economy or a company's fundamentals. Instead, it results from capital flows in and out according to various situations. (Therefore, in the short term, if you're a Value Investor, you'll need to endure even greater volatility than you've experienced in the past.)

When money flows into the investment world instead of the real economy, QE causes severe deflation rather than inflation. With the world turned upside down like this, where will the future lead us?

The global economy will face problems not from the devaluation of the large amount of printed money, but from the time bomb of public debt that has grown beyond manageable levels:

- The US has accumulated over $90 trillion in on and off-budget debt.

- Japan has $10 trillion in public debt.

- The Eurozone has over €12 trillion in public debt.

And every country's debt continues to increase with no signs of slowing down. (Remember, all the numbers above are from 2015)

What do most governments do about this problem?

When you need to borrow large sums from others, as governments worldwide are doing now, the best way to reduce your burden is to keep interest rates as low as possible.

Thus, global interest rates in this era are at rock bottom:

- The US has an interest rate of 0.25%

- Japan has an interest rate of 0%

- Germany has an interest rate of 0.05%

- Switzerland has an interest rate of -0.75%! (In other words, if you lend money to the Swiss government, you have to pay them interest!?)

Our world is increasingly approaching the era of NIRP: Negative Interest Rate Policy.

With low interest rates, governments borrow freely. But when interest rates remain low for many years, risks to the economic system follow. This is because there's only borrowing until debt becomes overwhelming and impossible to repay (both in the public and private sectors).

With high debt, the economy becomes fragile, and if any small problem arises, the debt bubble can burst at any moment. (For example, in Thailand during the Tom Yum Kung crisis, when the baht was floated, dollar-denominated debts doubled instantly, causing many private businesses to collapse.)

Back to US - interest rates this low for nearly a decade have led to significant dollar exports (lending) to various countries, especially developing country governments that have borrowed large amounts of dollars in recent times.

But US can't maintain such low interest rates for long. The first problem US will face is that state welfare funds will struggle with returns.

Normally, these funds must invest in low-risk assets, which inevitably means lending money to the government (i.e., buying government bonds). However, the very low bond yields put these welfare funds at risk of collapse, as they can't increase their capital base enough to cover future expenses in an aging society where welfare costs will increase exponentially.

This is not a minor issue. Many American citizens rely heavily on state welfare. US can't allow this situation to continue because it would destroy confidence in the government and could trigger a chain reaction.

Moreover, the FED's money printing hasn't caused the expected inflation because instead of the increased money supply circulating in the US economy, it has flowed out to speculate in markets worldwide. The economic stimulus hasn't worked as expected.

Even worse, while the US economy hasn't recovered as it should have, the stock market has been booming due to excess liquidity from money printing. (Money isn't injected into the real sector due to high risk, but into the stock market instead. The economy is bad, but stocks are rising.) This situation is similar to what happened in US before the Great Depression, when the FED lowered interest rates from 7% to 3% between 1921-1927, and Wall Street stocks soared for several consecutive years.

The FED thus faces two problems: It must prevent a bubble in US and help welfare funds survive to maintain public confidence, by "raising interest rates."

According to economic theory, when interest rates rise, businesses' and the government's financial costs increase, which should cool down the economy. Money will be absorbed out of the economic system. As interest rates rise, welfare funds will receive better returns, avoiding bankruptcy.

But the question is: Will raising interest rates really solve the problem? How are the FED's interest rates related to global capital?

I'll continue this story later.

QE and Inflation Theory (Part 4)

Capital Flow | July 2015

What is the main problem that follows the FED's interest rate hike?

I'm not talking about the increased cost of US public debt due to higher interest rates, because the US has never really cared about its debt burden (otherwise, they wouldn't have adjusted the debt ceiling dozens of times without hesitation).

It's the emerging market countries that have borrowed in dollars who will face the problem of a heavier debt burden due to rising interest rates.

Some economists believe that the US won't gradually increase interest rates gently. They might need to sharply raise interest rates in a short period. I somewhat disagree on this point, but if it does happen, countries that have borrowed heavily in dollars will certainly face major problems.

Previously, high debt burdens affected developed countries, but if interest rates rise sharply, in a few years, emerging market countries will face problems from rapidly increasing debt burdens. This will lead to high debt levels worldwide, unavoidably.

Imagine most emerging market countries in the world starting to face a situation like Greece is currently in - borrowing more and more, unable to pay off existing debts because payments only cover interest while the principal grows. The debt burden becomes even heavier as the dollar strengthens, requiring more payment when comparing dollars to their own currency.

I'll also talk about the bubble problem caused by capital inflows.

We've seen an example of this during The Great Depression in 1929. After years of low interest rates, the FED was pressured to raise rates to slow down the hot stock market and bubble conditions. Interest rates rose from 4% to 6%.

But surprisingly, the Dow Jones didn't cool down at all.

Wait, doesn't theory say that when interest rates rise, the economy should cool down because borrowing costs increase, making business expansion difficult? And when interest rates are high, some people will stop investing in stocks and put their money in banks instead?

How did the stock market double instead?

Some investors did stop investing and moved money from the stock market to bank deposits. But the proportion of that money was very small compared to the capital flow rushing back into US due to the interest rate hike. (When US lowered interest rates earlier, it was because the dollar was very strong and capital was continuously flowing into US. US tried to push capital flow back to Europe by reducing interest rates from 7% to 3% during 1921-1927, as I mentioned in the previous part.)

In 1927, when interest rates rose, more capital flowed back than was absorbed out of the system, causing the Dow Jones to make a new all-time high around 390 points before the bubble burst, leading to the most severe economic crisis in the country's history.

The Dow Jones collapsed from 390 points to about 40 points, or simply put, it fell by 90%. If you can't imagine what a 90% hell looks like, try to imagine if today's SET index collapsed like the Dow Jones during The Great Depression - the SET would fall from 1,500 points to 150 points, much worse than during the Tom Yum Kung crisis!!

And the capital flow in this era is much more massive than in 1929.

And the capital flow in this era is much more liquid than in 1929.

When large amounts of money flow into US, another consequence will be the value of the dollar. When a large country like the US raises interest rates, while Europe still faces uncertainty regarding debt issues, capital is likely to start flowing out of Europe and into the US more. The dollar is likely to strengthen significantly.

If the dollar strengthens, US will start to face problems similar to Japan in 1985. One of the reasons that caused the economic bubble to burst, causing Japan to collapse and not recover since then, also came from capital flow. I'll explain this to you.

Before 1985, Japan's economy was very prosperous. After reforming itself following defeat in World War II, during that time the Japanese currency was weak and the US dollar was strong. (In the 1980s, there was a global inflation crisis due to the Iranian Revolution, causing oil prices to skyrocket. The US had to suddenly raise interest rates to nearly 20% to save the dollar's value, causing the US dollar to strengthen rapidly, as I mentioned in previous parts.)

This led to Japan's exports growing for several consecutive years, along with new innovations from Japan that sold well worldwide, including cars and electrical appliances. During that time, Japan's economy looked very promising, and the stock index was extremely hot.

After losing World War II, in 1950, the Nikkei newspaper (Nihon Keizai Shimbun) began calculating the Nikkei index by using 225 large stocks on the Tokyo Stock Exchange (similar to Thailand's SET50).

The Nikkei index started in 1950 at 100 points, like other global indices. After 35 years, the Nikkei rose from 100 points to over 10,000 points, a 100-fold increase! (Compared to Thailand's SET, which went from 100 to 1,500 points in 40 years)

In contrast, when US successfully fought to save the dollar, it came at the cost of economic downturn due to higher interest rates and a stronger dollar.

Many people believed that Japan would overtake the US as the world's largest economy, especially since US was just recovering from the inflation crisis and was still unstable.

US couldn't accept this. Japan, its own protégé, was about to become the world's number one, clearly stepping on US’ toes.

As a result, Japan was pressured by the US through the Plaza Accord to strengthen its currency by half (in simple terms, the dollar weakened by 50% against the yen unnaturally - try Googling "Plaza Accord", it's an interesting topic that many Thais aren't familiar with).

In 1985, 1 dollar exchanged for 260 yen. After the Plaza Accord, within 3 years, 1 dollar exchanged for only 120 yen! A brutal change.

As the yen began to strengthen rapidly, a shocking problem arose from the same culprit: capital flow!

Global capital flooded into Japan violently, like a barrage of arrows raining down on Japan. The already hot Nikkei market became even hotter, rising from 10,000 points in 1985 to an all-time high of 38,916 points in 1989, nearly a 4-fold increase. This was Japan's bubble state, caused by capital flow. (It's hard to imagine what it would be like if the SET index went to 38,000 points.)

This was contrary to Japan's fundamentals. Japan became rich through exports, benefiting from a weak currency. When the currency strengthened by half, their products didn't sell as well as before. The real sector was beginning to face problems, but the stock market was running in the opposite direction, in an extreme blood frenzy.

When the conflict reached its peak, Japan's economic bubble in both the stock market and real estate eventually entered a collapse cycle. The Nikkei bubble burst, ending the prosperity of the world's second-largest economy. Nearly 30 years have passed since the Plaza Accord, and Japan still hasn't recovered.

This is the frightening aspect of capital flow, which is like a time bomb that could explode after the US raises interest rates.

This is the frightening aspect of capital flow, which is like a time bomb that could explode after the US raises interest rates.

Warning: I'm not saying that after raising interest rates, the American stock market will become as hot as the Nikkei was back then. Don't rush to buy American stocks after reading my article.

We can't say for certain that history will repeat Japan's bubble period, because many factors in today's American economy are very different from Japan's at that time. Japan's economy then was very strong due to the country's fundamentals. When capital flowed in, the stock market became even hotter. But US now is not in the same situation. The economy is still very fragile, clearly different from Japan at that time.

However, when the dollar strengthens due to capital flow, global deflation will intensify. Various commodities may fall, contrary to the dollar's movement (gold, oil, etc.). As deflation worsens, American citizens will start facing problems, and the economy will struggle to recover, even though the stock market might soar due to capital flow.

The government will need to try to increase revenue by squeezing every bit of tax (this is another reason why money in the future might be in electronic form, allowing governments to control the flow of money and taxes down to the last cent without any leakage).

The US’ enormous debt burden and money printing won't cause any problems as long as US can maintain public "confidence".

But when citizens start suffering more and confidence diminishes, that's when disaster will strike. All the past sins, including money printing and debt, will come back to haunt them.

Hyperinflation doesn't occur due to money printing, but due to a severe loss of confidence in the government. Small countries like Zimbabwe experience hyperinflation when they print money because people immediately lose confidence in the government. But US can print money as long as people still have confidence.

This interest rate hike, in the short term, seems to be building confidence, making people believe that US is back and the economy is recovering. But in the long run, it might trigger several things that could destroy American people's confidence in their government. That's when the US economic crisis will follow, and the time bomb of US debt burden will start ticking. But this is unlikely to happen soon. It probably won't be less than 5-6 years from now.

This timing might coincide with the period when the yuan and China will have strengthened and be ready to rise fully. The world's economic superpower may start changing hands during that time.

I've written these four long parts to show how deflationists view things differently from inflationists. Interest rate hikes, capital inflows, and currency values have a deep, dynamic relationship with each other, while money supply is considered a less significant variable.

I used to be an inflationist years ago, but the results of the global economy from the QE era to the present made me start changing my mind. Eventually, I studied deflationist theories and combined knowledge from both schools. In the short term, deflationists will be more accurate, but in the long term, I believe inflationists will be correct (unless a war resets the global economy first).

In the long run, everything will reflect reality. If you print money recklessly, ultimately the currency will depreciate. But what people often misunderstand is that the currency won't depreciate due to the large amount of money printed, but from the long-term decline in confidence in the country.

In the short term, it's different. People who believe in hyperinflation love gold. I used to love gold too. But now I believe that this year, gold might have a chance to fall heavily below $1,000 per ounce due to the strengthening dollar (I see this as a buying opportunity, towards the end of the year, if it really falls below $1,000 per ounce).

I'm not making definitive predictions, just exchanging ideas to give you another perspective on the world. Think and analyze. I could be wrong. We'll have to wait and see.

But what I want to point out is that interest rates in the economic system are not just about controlling borrowing costs for the public and private sectors or absorbing money supply in the system as we used to understand from textbooks.

Interest rates are one of the variables that will cause capital flow, which will affect the global economy in the era of globalization. As capital flow increases exponentially due to money printing, the picture of economic theory we used to understand becomes more and more distorted. We need to understand and keep up with it.

I've written quite a lot. I can end it here. Thank you very much for reading and following along.

When Technology will Destroy Humanity (Part 1)

Rise of the Robot | December 2016

You're not misreading the title. This is indeed an economics article. The changing structure of human and machine labor in the coming decade is likely to create massive problems for the global economic system. As automated systems like robots, and breakthrough technologies like blockchain and artificial intelligence, will make human labor 'surplus' to the economic system.

What will happen in a future world where production and services can be driven without the need for humans?

In my personal opinion, this leaping technology won't destroy humans like Skynet in Terminator or the Machines in The Matrix. But it will destroy the traditional economic structure we have, making the future economic system drastically different from the one we're familiar with.

Let's look at the trends and see how the chain reaction of the technological revolution will affect the global economic system in the coming decades.

Employment Crisis

It's clear that the next generation will face problems finding jobs. By the time they reach full working age, there will be few jobs left that they can do.

Industrial robots are about to replace young factory workers. This trend has already begun. For example, South Korea has a ratio of 4.78 robots per 100 human workers, and this number is likely to increase with the development of robots and lower costs. (Remember that one robot might replace up to 100 humans, so every 1 unit increase in robots will reduce human labor by more than 1 unit.)

2024 Update

As of 2024, the global trend in industrial robotics shows a significant rise in robot density, with the average in manufacturing reaching 1.51 robots per 100 human workers, a figure that has more than doubled in six years.

The US has 2.85 robots per 100 human workers, while South Korea leads with 10, followed by Singapore (6.70) and Germany (4.15). China has notably surpassed the US, achieving a density of 3.22 robots per 100 workers, ranking fifth globally.

This increase reflects substantial investments in automation, with China's rapid growth marking it as the fastest-growing robot market. Industrial robots, including Autonomous Mobile Robots (AMRs) and collaborative robots (cobots), are increasingly utilized for material handling and assembly tasks, and Robotics as a Service (RaaS) is making these technologies more accessible.

Despite concerns over job displacement, the rise in robotics is also creating new opportunities in maintenance, programming, and IT security

Sources:

- https://www.enterpriseappstoday.com/stats/robotics-industry-statistics.html

- https://ifr.org/ifr-press-releases/news/global-robotics-race-korea-singapore-and-germany-in-the-lead

- https://www.chinainternetwatch.com/42913/china-outpaces-us-robot-density/

- https://www.ctemag.com/news/china-overtakes-united-states-robot-density

Autonomous vehicles will cause taxi and transport drivers to lose their jobs. Next year, driverless public vehicles will begin service in many countries, including Singapore, UAE, and Japan. Drones might replace postmen. Automated trains have long existed in Japan. Future transport systems will be able to operate without humans at all.

Construction jobs that used to require many workers aren't being replaced by robots carrying bricks and cement. It's worse than that because the traditional construction system is being replaced by giant 3D printing systems already in use in China and the USA, which can build a house in less than 24 hours.

In the future, smart farm systems using IoT, Blockchain, and robots will be able to create agricultural products from plowing to harvesting without relying on farmers at all.

Have you heard of cultivated meat technology? Lab-grown meat that scientists, funded by Google co-founder Sergey Brin, are researching can produce animal meat from stem cells without raising a single animal. While this technology may help solve the world's food shortage crisis in the future, the livestock farming profession (which causes significant pollution to the world) may disappear as well.

2024 Update

As of 2024, the cost of producing cultivated meat has significantly decreased compared to its early stages. For example, Future Meat Technologies has managed to produce cultivated chicken breast for approximately $66 per kilogram. This is a hybrid product that blends plant proteins with cultivated meat. Other companies, such as Shiok Meats, have also achieved cost reductions, planning to lower the production costs for their cultivated prawn to $50 per kilogram, with further aims to reduce it to $5 per kilogram in the future.

Overall, the current cost of producing cultivated meat varies widely depending on the company and type of meat, ranging from around $66 to $22,423 per kilogram.

According to the Good Food Institute, the cost of producing cell-based meat could drop to around €4.68 per kilogram ($5) by 2030 if manufactured at scale. This cost is expected to match the price of conventional meat, representing a major milestone for the mass adoption of sustainable protein alternatives.

In the present scenario, cultivated meat is more expensive due to the complexities involved in the production process, including the development of cost-effective cell culture media and bioreactor technologies. However, advancements in technology and scaling up production are anticipated to reduce costs over time.

Sources:

- https://goodseedventures.com/cultivated-meat-production-costs-past-present-future-2/

- https://reason.com/2021/03/11/cultivated-meat-projected-to-be-cheaper-than-conventional-beef-by-2030/

- https://link.springer.com/chapter/10.1007/978-3-031-55968-6_21

- https://www.foodnavigator.com/Article/2021/04/21/Cultivated-meat-to-reach-price-parity-with-conventional-meat-by-2030-but-will-it-win-the-green-argument

The use of Blockchain and electronic money systems will significantly reduce the number of financial and banking personnel, as well as gradually decrease the number of bank branches.

Deep learning technology used to create increasingly intelligent chatbots will replace more than 90% of customer service and telemarketing jobs (the remaining 10% involving complex issues will still require humans).

Even service jobs that we expect robots to have difficulty replacing will be affected by outsourcing to countries like India or Africa, where the working-age population will grow to its peak in the next 20 years. (Based on birth rates, India will surpass China as the world's most populous country.) Virtual Reality technology, which will develop rapidly in the next era, will allow us to provide cross-continental services without physical presence. High-wage countries like the US, European countries, or Japan will face increasing outsourcing of labor to cheaper sources.

This technological change is likely to be even more intense than the Industrial Revolution following the discovery of coal in the 18th century. The Industrial Revolution created many jobs for humans, while the technological revolution in the next decade will do the opposite.

From states that used to only assist retired and disabled populations, they will now have to bear an additional burden of helping unemployed working-age populations.

Of course, our primary concern about modern technology replacing the workforce is the rapidly increasing unemployment rate in developed countries. In reality, this dramatic change will have a continuing impact not only on the working population but also on the retired population, and ultimately may be severe enough to destroy the stability of the state.

This leads to the next chain reaction towards an aging society.

Social Security Crisis

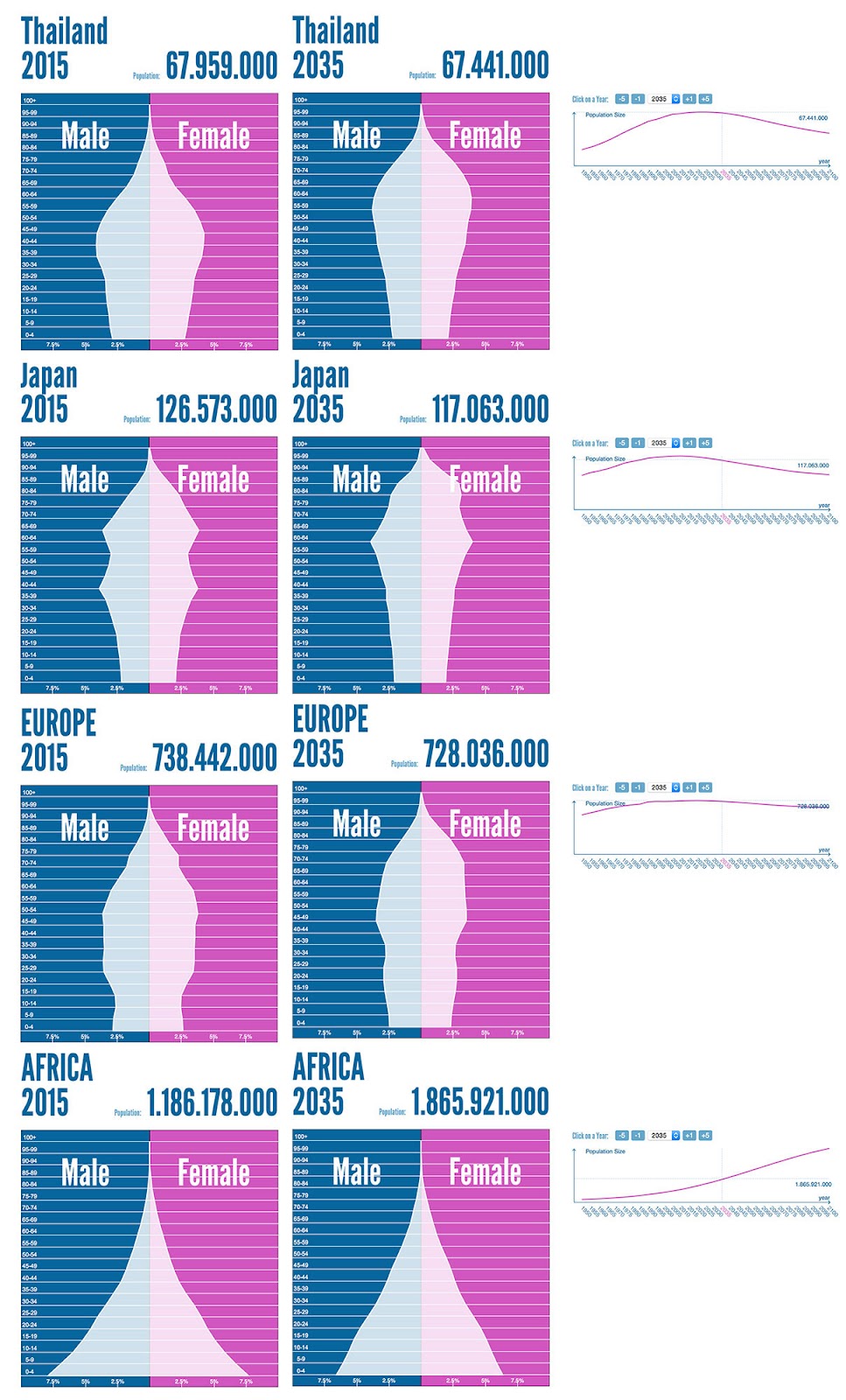

The issue of an aging society has been discussed for a long time. According to the populationpyramid website, it's estimated that by 2100, Thailand's population will decrease from 68 million to around 40 million (-41%), while Japan's population will decrease from 127 million to just 83 million (-34%).

While most developed countries are experiencing population declines due to very low birth rates from modern values that don't favor having children, and low death rates from advances in medical technology, African countries are seeing rapidly increasing birth rates. This leads to vastly different future population structures across continents.

Imagine a scenario in developed countries where working-age people are unemployed, causing the government to lose tax revenue, and social security system income to significantly decrease.

Additionally, they face the problem of an increasing retired population. As fewer people are born and more become unemployed, the state loses income, while the retired population increases.

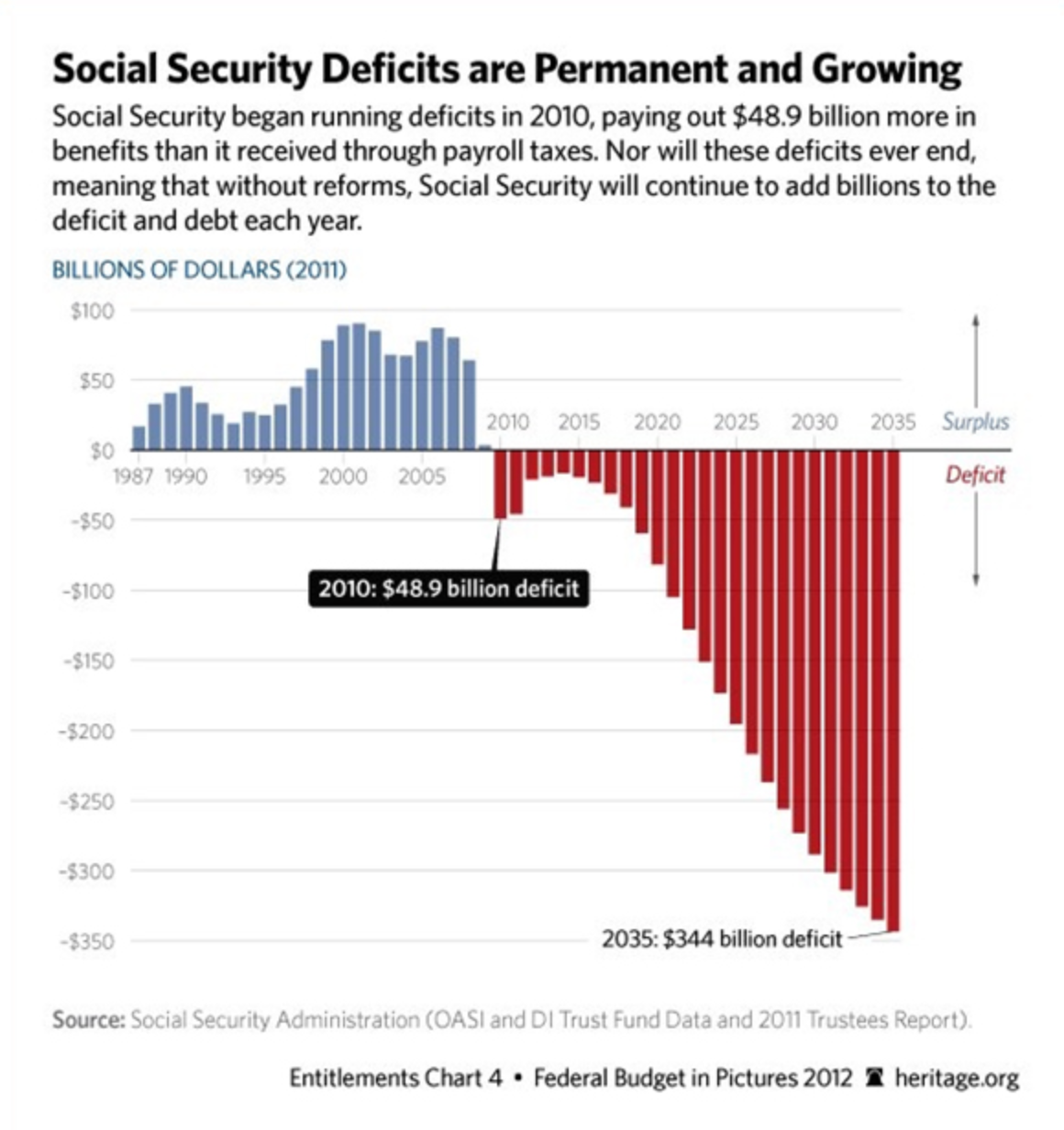

The US Social Security Trust Fund has been experiencing negative cash flow since 2010 (income collected from the working-age population is less than expenses paid to the retired population, resulting in a budget deficit). It's projected that the $2.7 trillion social security fund may be completely depleted by 2030 (this estimate doesn't account for the acceleration of technological development that will increase unemployment in the working-age population in the next decade).

Another burden for social security funds in developed countries is that the fund needs to seek low-risk returns. Most social security funds tend to lend to the government by purchasing bonds. US Social Security has long been a major creditor to the government, holding nearly 100% of its fund in US bonds ($2.7 trillion). It's the government's number one creditor, accounting for about 14.4% of the $19 trillion debt, more than the amount of US bonds held by Japan and China combined! (However, in the long term, if the US government continues to spend money like paper, the FED might become the number one creditor instead.)

However, global interest rate trends are continuously decreasing, to the point where some countries have negative bond interest rates (Switzerland, Japan, Germany). This means that creditors like social security not only receive lower returns but also face situations where the principal decreases due to negative interest rates. This is a large time bomb hidden in the social security systems of almost all developed countries. (In my personal opinion, the FED needs to raise interest rates because of the pressure from this bomb; I don't give much weight to the economic recovery narrative.)

With drastically decreasing income, rapidly increasing expenses, and funds yielding rock-bottom returns, if this continues, social security systems in developed countries worldwide will eventually go bankrupt. (It's estimated that the US Social Security system will go bankrupt within the next 10-20 years.)

The question is, how can the social security system survive?

- Increase saving? This is extremely difficult to nearly impossible. When people don't have jobs, how can social security generate saving?

- Reduce expenses? This is somewhat possible. With rapidly advancing technology, healthcare costs might decrease significantly. However, a major obstacle is that most giant businesses in the healthcare sector are not charitable organizations and likely won't help the state reduce costs easily.

- Increase investment returns? This comes with risks, namely that social security funds will abandon government bonds and move money into other assets with potentially higher returns, such as stocks or corporate bonds.

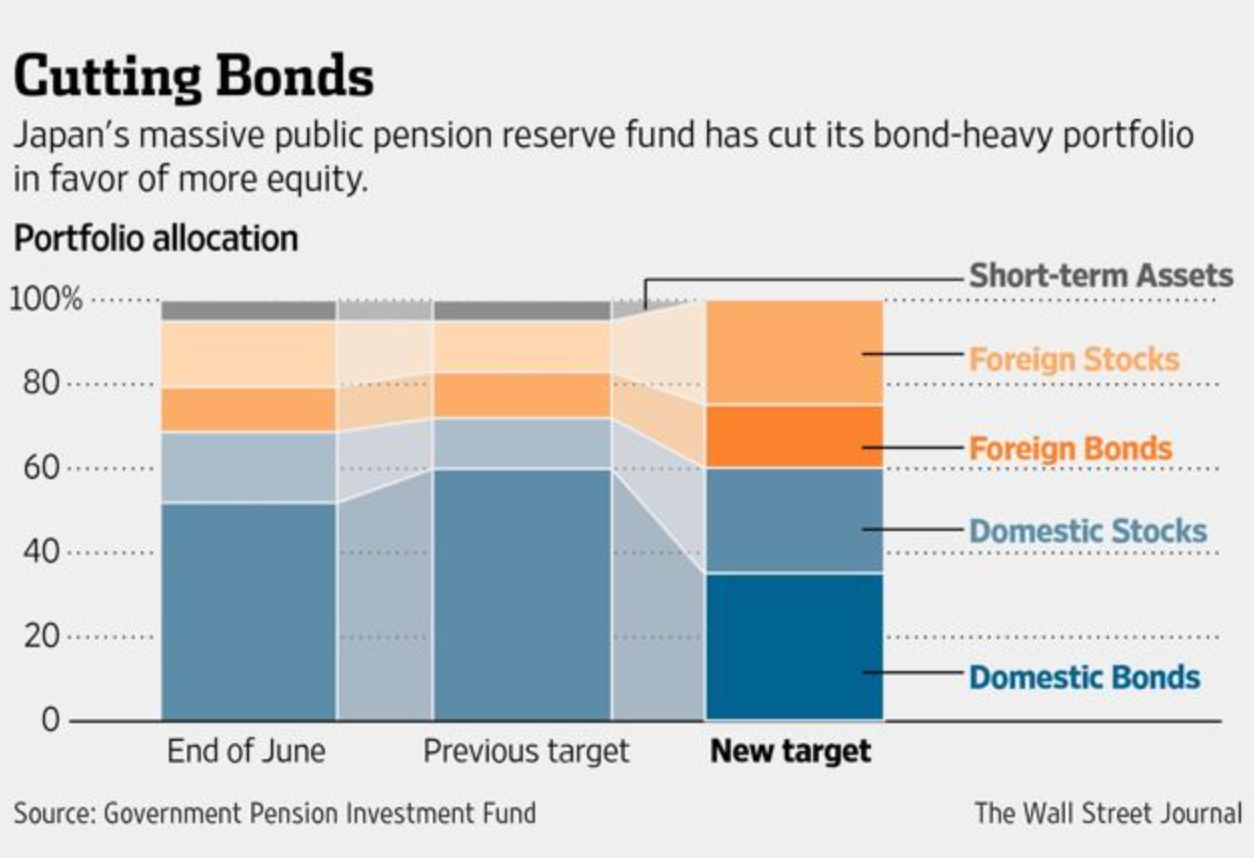

An example of this solution was seen in 2014 when Japan's social security fund (GPIF: Government Pension Investment Fund), with assets of $1.2 trillion, reduced its government bond holdings and increased its investment in Japanese stocks from 12% to 25%, or moving to hold stocks for up to a quarter of the fund! (This was one reason why the Nikkei rose significantly during 2014-2015.)

But of course, this decision inevitably 'increases risk' for the fund. If the stock market crashes, it means people's money will disappear immediately. (The Nikkei's market cap decreased by nearly 30% from late 2015 to mid-2016, and naturally, GPIF's central fund decreased accordingly to some extent.)

Let's look at the equation: (2) = (1) + (3).

If (1) decreases faster than (2), the only choice is to increase (3).

Theoretically, there are only two ways to increase fund returns: abandon bonds or increase returns on new bonds by raising interest rates, or perhaps do both.

Both ways will lead to the third chain reaction: the Sovereign Debt Crisis, which could be an even bigger bomb that might follow. I'll talk about this in Part 2 because I've written quite a lot already, and this part is getting too long.

PS. Some might wonder why, when GPIF abandoned Japanese government bonds for stocks, the yield on Japanese bonds didn't spike but instead plunged even lower (at that time). Who bought the bonds that GPIF dumped? In fact, it was the Bank of Japan (BOJ) that controlled the yield curve of bonds by buying up the bonds that GPIF dumped (BOJ's bond-buying program). It's similar to how the FED prints money for the US government to spend. In Japan, the BOJ prints money to buy government debt from GPIF. Central banks of superpower countries playing like this in the long term might lead to a severe bond crisis.

2024 Update

The Social Security trust funds are facing a significant long-term deficit, but the outlook has improved slightly compared to last year's projections:

- The combined Social Security Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) trust funds are now projected to be depleted in 2035, one year later than previously estimated.

- Upon depletion of the trust fund reserves in 2035, the program will still be able to pay 83% of scheduled benefits using ongoing tax revenues, declining to 73% by 2098.

- The 75-year actuarial deficit for the combined Social Security trust funds is now projected at 3.50% of taxable payroll, down from 3.61% in the prior year's report.

- This improvement is primarily due to stronger-than-expected economic performance and lower projected disability incidence rates, partially offset by a lower assumed ultimate birth rate.

- However, Social Security still faces large and growing cash flow deficits, projected at $3 trillion over the next decade, equivalent to 2.3% of taxable payroll or 0.8% of GDP.

- Policymakers have limited time to enact reforms to restore solvency to the Social Security system before the trust fund reserves are depleted, at which point across-the-board benefit cuts would be required.

In summary, while the Social Security outlook has improved slightly, the program still faces significant long-term financing challenges that require legislative action to address.

Sources

- https://www.ssa.gov/policy/trust-funds-summary.html

- https://www.crfb.org/papers/analysis-2024-social-security-trustees-report

2024 Update

Updated information for 2023: GPIF reported record-breaking performance of $133 million in Q2 2023, following the Nikkei index's climb from 16,000 points in 2014, when GPIF adjusted its investment allocation from bonds to more stocks, to a new all-time high of 40,000 points in 2024. This is considered one of the best decisions made during the era of the late Prime Minister Shinzo Abe, known for his economic policy "Abenomics".

When Technology will Destroy Humanity (Part 2)

Sovereign Debt Crisis | December 2017

In the first part, I discussed how technology, along with changing population structures, will cause two major problems:

Employment Crisis: Working-age people will lose jobs due to technological disruption.

Social Security Crisis: Retirees will face a social security crisis, potentially leaving no money for the elderly in their later years.

In this part, I'll discuss the third crisis: the Sovereign Debt Crisis. I'll briefly explain the debt structure of major powers like the US, Eurozone, and Japan.

Sovereign Debt Crisis

How is government debt a crisis? I'll try to explain the bond issue in layman terms.

Typically, a country's income comes from taxes, collected by the Treasury in various forms. When there's income, there are expenses, which involve government expenses.

If treasury income exceeds expenses, it's called a budget surplus.

If treasury expenses exceed income, it's called a budget deficit.

Imagine if a country were like a company. When income is less than expenses, the company would face a cash shortage. The solution to this shortage is "borrowing money".

It's the same for countries. When they run large budget deficits, they eventually run out of money. The government then needs to find more money to continue operations. The easiest way is to borrow money. Governments borrow by issuing bonds.

Many ask, "Why overspend? If you have little income, spend less to avoid debt." But governments aren't companies. In today's capitalism, running budget deficits is almost normal for governments worldwide. This is because modern economic thinking (Neo-Keynesian) believes that budget deficits can help countries grow well.

In simple terms, Neo-Keynesian economists (like Paul Krugman) believe that when the economy is sluggish, the government needs to intervene and create jobs by increasing government spending to drive the economy while improving the country's infrastructure. So in the short term, the money the government overspends will be used to build, build, and build - whether it's high-speed rail, roads, ports, irrigation systems, highways, etc.

These massive projects will, in the short term, create economic circulation (the government creates jobs when the private sector is weak). In the long term, this infrastructure will increase the country's competitiveness, reduce private sector business costs, and improve international competitiveness. As the economy improves, the government will receive more tax revenue in the future, can run budget surpluses, and use the excess to offset past deficits.

This idea sounds good, following John Maynard Keynes, the father of Keynesian Economics, who helped the world escape the deflation trap during The Great Depression in 1929 through government intervention and injection.

But in the present era, it's not working out that way! (The failure of Neo-Keynesian economics is a long story that I won't cover in this post. If there's a chance, I might try to explain it in the future.)

US Debt

Major world powers have been running budget deficits every year, stimulating their economies for decades since the post-Bretton Woods era when the US abandoned the gold standard. Government spending has increased exponentially. (If you're wondering why government spending is related to abandoning the dollar-gold peg, I recommend reading "Why Bitcoin Surpassed $1,000: Explaining Cryptocurrency from an Economic Perspective")

Many ask, "Why overspend? If you have little income, spend less to avoid debt." But governments aren't companies. In today's capitalism, running budget deficits is almost normal for governments worldwide. This is because modern economic thinking (Neo-Keynesian) believes that budget deficits can help countries grow well.

In simple terms, Neo-Keynesian economists (like Paul Krugman) believe that when the economy is sluggish, the government needs to intervene and create jobs by increasing government spending to drive the economy while improving the country's infrastructure. So in the short term, the money the government overspends will be used to build, build, and build - whether it's high-speed rail, roads, ports, irrigation systems, highways, etc.

These massive projects will, in the short term, create economic circulation (the government cThe US has been issuing more and more bonds, but it's never enough for government spending. Eventually, they resorted to having the Federal Reserve "cheat" by using QE to print money to buy US bonds - in simple terms, printing money for the government to use. This includes keeping interest rates low to reduce the government's interest expenses. (Some say the government lowers interest rates to stimulate the economy, but in reality, it doesn't help the economy much; it mainly helps reduce government debt burden)

A surprising problem with capitalism is that no matter how much debt the government accumulates, everyone still believes the state has good credit, so bond interest rates remain low. (Except for smaller countries with poor credit like Greece, which once had bond interest rates soar to over 20%, indicating a lack of trust in the Greek government.)

The US government has a public debt approaching $20 trillion (in 2016), but whenever the government needs money, they just raise the debt ceiling. Since 1962, the US debt ceiling has been raised 74 times.

Imagine if the government were a person with a limited income of $15,000 per month but spending $50,000. They'd solve this by using credit cards every month, and when the credit limit is reached, they'd ask the bank to increase it 74 times. If you were the banker, you'd blacklist this person and try to get all the principal back as soon as possible.reates jobs when the private sector is weak). In the long term, this infrastructure will increase the country's competitiveness, reduce private sector business costs, and improve international competitiveness. As the economy improves, the government will receive more tax revenue in the future, can run budget surpluses, and use the excess to offset past deficits.

This idea sounds good, following John Maynard Keynes, the father of Keynesian Economics, who helped the world escape the deflation trap during The Great Depression in 1929 through government intervention and injection.

But in the present era, it's not working out that way! (The failure of Neo-Keynesian economics is a long story that I won't cover in this post. If there's a chance, I might try to explain it in the future.)

But with the US government, it's the opposite.

Now, with high debt and long-term low interest rates, problems are emerging. The largest creditor of the US is its own Social Security fund. The fund buys government bonds, or in other words, the government is using people's money and paying rock-bottom interest. As I mentioned in the previous post, this puts the Social Security fund at risk of bankruptcy. (I believe this is the deep reason why the FED is forced to raise interest rates.)

I'll leave this issue here about how the US future will look with such overwhelming debt, and move on to talk about Eurozone debt.

Eurozone Debt

The Eurozone is facing a debt crisis no different from the US, perhaps even worse due to chronic economic problems from the half-hearted Eurozone integration. Eventually, the ECB (European Central Bank) had to imitate the US by printing money (QE) to buy government bonds, or in plain terms, print money for state use.

The ECB has been printing money for several years now, to the point where the ECB now holds a higher proportion of Eurozone bonds than the BOJ holds of Japanese bonds or the FED holds of US bonds.

At the end of the year, there was news that the ECB plans to reduce and stop QE.

What happens after ECB stops QE?

Currently, the ECB holds 40% of all Eurozone government bonds!

The ECB has been buying bonds at a rate 2.5 times higher than the bonds issued by European governments in a year, setting a record among all countries that have implemented QE. This chart clearly indicates how severe the European crisis really is.

If ECB stops printing money, there won't be funds to buy more bonds.

The question is, who will buy European government bonds after the ECB?

Bond trading is similar to stocks. If there are no bids for stocks, the stock price plummets. Similarly, if there are no bids for bonds, the bond price drops (and yields soar, as happened with Greek bonds before).

Therefore, the ECB must have a backup plan if they truly intend to stop QE. How can they make the accumulated low-quality government bonds attractive to buyers?

The ECB is currently pushing a proposal to issue Eurobonds!

It sounds impressive and credible.

But in reality, Eurobonds are like bundling together both good and bad bonds from various European countries, repackaging them, and calling them Eurobonds. It's similar to what happened during the US subprime crisis when subprime mortgages were bundled into MBS, and then MBS were bundled into CDOs. It's like mixing rotten eggs with normal ones and selling them at a deceptive price. Financial experts call this process "Securitization," which nearly destroyed the US economy.

No matter how you dress up something rotten, it remains rotten inside. Eurobonds (if they materialize) are just a way to postpone Europe's problems. When the truth is known and no one wants Eurobonds anymore, it will explode like the subprime crisis did.

In conclusion, the ECB has announced an indefinite extension of QE (even if at a reduced amount), buying more time for the Eurozone.

It's strange that European stocks and the euro have rallied this year, while the dollar has continuously weakened (which I incorrectly predicted would be short-lived before strengthening again, but it has been ongoing for months now). This is despite the fact that I haven't seen any real improvements in Europe since the 2011 problems.

Personally, I still believe the current strengthening of the euro is just a short-term illusion. I don't think Europe has recovered (at a fundamental level). All the problems the Eurozone had before are still present and have even worsened.

The Eurozone's problem is its half-hearted integration - unifying the currency while keeping each country's debt separate. Each country has its own bonds with different credit ratings, all traded in euros.

In my opinion, the only way to fundamentally solve the Eurozone debt crisis is to consolidate all Eurozone countries' debts into a single euro debt - not just future debt, but all past debt, ready for potential devaluation. But this is likely impossible, especially as Germany would certainly oppose it.

Let's pause on the Eurozone debt issue and conclude with Japan's debt.

Japan Debt

I'll briefly discuss Japan's debt as it's not much different from the US and Eurozone. Japan has been overwhelmed with debt from ineffective economic stimulation for nearly 30 years, trying to pull the country out of chronic deflation (an interesting economic issue I might discuss in future posts if I have enough writing energy).

In my previous post, I mentioned that Japan's social security faced low returns from holding government bonds, forcing them to shift their portfolio from bonds to stocks for higher returns.

The phrase "abandoning bonds" is scary. Let me give a simple example:

Imagine you lend money to a friend. When you no longer want to be a creditor (due to low returns, poor credit, or any reason), you'd rush to sell the debt to someone else as quickly as possible.

When you're in a hurry to sell debt, you need to lower the price. As the debt price decreases, the interest rate increases relative to the discounted selling price. For example, a 100 baht debt with 1.5% interest rate, if sold at 90 baht due to fear of default, would effectively increase the interest rate to 1.67%.

You're like Japan's social security fund, and your debtor is the Japanese government.

Typically, if you sell bonds, the bond yield increases (indicating higher risk, like Greece's bond yield exceeding 20%), as people rush to sell bonds at lower prices.

This is the phenomenon we often hear about as "surging yields" - it's actually the bond selling price decreasing. The more bonds are sold cheaply, the higher the yield surges.

Strangely, Japanese bond yields have remained consistently low, occasionally spiking slightly before returning to normal levels.

Does this mean Japanese bonds are trustworthy?

Actually, it's the opposite. The reason people are abandoning Japanese government bonds without yields increasing is because the Bank of Japan (BOJ) is cheating the game!

BOJ has a Bond Buying Program, essentially unlimited QE to buy government bonds that people are dumping, keeping yields artificially low.

This is extremely unfair!

In the long run, if many people abandon government bonds, BOJ will end up like the ECB, becoming the government's primary creditor! (Currently, Japanese citizens are the government's main creditors, but they're starting to struggle holding government bonds as they retire and need to sell bonds for living expenses, or working-age people shift to other investments due to low bond returns.)

This is a dangerous signal, indicating that the state has lost credibility, and no one wants to lend to the government, forcing the central bank to shoulder this burden.

(Those who've read my Bitcoin articles will start to see why cryptocurrencies are gaining credibility. Investors are losing faith in the public sector and seeking alternative investments. Cryptocurrencies, being "independent" from the state, are growing rapidly and intensely. These two phenomena occurring simultaneously is no coincidence.)

The central bank becoming the state's largest creditor signals that these superpowers' central banks cannot stop printing money!

If they stop printing money, there won't be money to lend to the state. Without money to lend to the state, it's game over - government bankruptcy, no money, no more loans, inability to repay principal, ending in default, loss of credibility, and a global chain reaction.

Many think a Sovereign Debt Crisis for superpowers will never happen, that the dollar will never collapse, that the US government can perpetually create debt.

In my next post, I'll share my hypothesis on how the emergence of technologies like cryptoassets and cryptocurrencies could shake the government bond market and accelerate the public debt crisis.

This is getting long, so I'll continue in the next post…

Why Bitcoin Surpassed $1,000

Explaining Cryptocurrency from an Economic Perspective | January 2017

Disclaimer: I have been a Bitcoin miner since 2013 and have consistently invested in Bitcoin over the past 3-4 years. As such, I have directly benefited from Bitcoin's price appreciation.

Welcoming the new year of 2017 with Bitcoin prices surpassing $1,000 for the first time in several years, I've noticed many people rekindling their interest in this electronic currency. Along with this renewed interest comes the common question: "Why is electronic money trustworthy?" So, I've decided to offer an economic perspective on Bitcoin to enhance understanding for the general public, providing a clearer picture of this electronic currency.

Remark - The explanation of the origin of money at the beginning is partially paraphrased from the article "What is Money" by NexttoNothing from Thaigold.info

To make this as easy to understand as possible for the general reader, I'll try to avoid complex technical terms and use analogies for easier comprehension.

To answer the question "Why Bitcoin?", we should start with the pain points of the current financial system. (I'll incorporate some economic theory to enhance understanding where appropriate.)

What problems does "money" currently have, and how can Bitcoin (under Blockchain technology) solve these issues? Let's explore.

"Money" - what most people in the world desire most. But what is it really?

The Meaning of Money

In reality, "money" has no intrinsic value. It's merely a medium of exchange. Without exchange, money wouldn't be important to humans; it would just be ink-stained paper with a number like 1,000 baht written on it.

Let's take a time machine back to the era before "money" was used, to better understand its origins and evolution from past to present.

In the past, due to production limitations, one person couldn't produce all the necessities for living. This led to the formation of social groups and the beginning of "division of labor", allowing individuals to focus on what they were "good at" to maximize production efficiency.

I cannot raise animals and grow rice simultaneously, so I raise cattle while you grow rice. When I need rice, I exchange my beef for your rice. This is the basic origin of resource exchange. In ancient times, there was no buying and selling of goods, only exchange. We call this system of exchanging goods for goods the "Barter System".

The Barter System had many problems. For instance, if my cattle weren't grown yet but I wanted to eat rice, I had nothing to exchange. I'd have to starve until I had beef to trade, which could mean starving to death.

Humans therefore devised a solution by finding a medium of exchange to represent resources. This medium of exchange needed to be accepted by the majority of society and had to be something that was "scarce", "non-counterfeitable", and "divisible into smaller units".

Gold and silver struck the jackpot as universally accepted mediums of exchange in ancient times. Their scarcity and the arduous process of extraction from tons of rock made them ideal candidates. Difficult to counterfeited materials. These precious metals could be melted down and divided into smaller units while maintaining their inherent properties.

This quality set gold apart from diamonds in terms of practical money. While diamonds are also scarce and difficult to forge, our ancestors didn't favor them as a medium of exchange. The reason? Diamonds can't be easily divided into smaller pieces like gold, and each stone's quality varies, making them impractical for everyday transactions.

The Birth of Gold Certificates

Gold served as "money" for millennia until the next evolutionary step. To avoid the inconvenience of carrying heavy gold or cutting it into tiny pieces for small purchases, gold storage businesses emerged. These businesses, the precursors to modern banking systems, would issue gold certificates to depositors.

These certificates gained acceptance as gold equivalents. Holding a certificate was as good as having gold in hand. People used these certificates for shopping, and merchants could either exchange them for gold or use them for further transactions.

As global trade flourished and world GDP increased, gold certificates became widely used. Eventually, it became impractical to exchange certificates for physical gold, as people primarily used them to acquire goods and services for daily life.

While actual gold lay dormant in vaults, gold certificates circulated worldwide. However, certificates from different countries often caused issues in international trade. This led to the development of standardized gold certificate systems. Each country had its own name for these certificates: "dollars" in the United States, "pound sterling" in England, "yen" in Japan, and "baht" in Thailand.

Exchange rates emerged:

1 dollar certificate could be exchanged for 100 yen certificates

1 pound sterling certificate could be exchanged for 50 baht certificates

Regardless of their form, all these certificates could be exchanged for gold in their issuing countries. This marked the beginning of our current "foreign exchange" system.

The Dollar's Liberation in 1971

The roots of our current monetary issues can be traced back to the Vietnam War era. The United States, heavily invested in the conflict, nearly depleted its dollar reserves. In a controversial move, the US government began printing more dollar certificates than it had gold to back them up.

Imagine if one gold bar typically backed one certificate. The US had 1 million gold bars but printed 5 million certificates - a fivefold overprint. This excess printing raised suspicions among other nations, who began to doubt the US's financial integrity. Countries like West Germany, Switzerland, and France started requesting gold in exchange for their dollars.

Faced with this dilemma, the US took a drastic step. On Friday, August 13, 1971, President Richard Nixon announced the severance of the dollar's tie to gold. This meant the government could print currency without gold backing, and dollar holders could no longer exchange their notes for gold. The dollar was now "free."

This event, officially known as the end of the Bretton Woods System and nicknamed the "Nixon Shock," marked a turning point in global finance.

This decision triggered worldwide financial turmoil. Governments began printing money without restraint. Some countries with poor credit, like Zimbabwe, faced economic collapse due to excessive printing. However, nations like the US, Japan, UK, and Eurozone countries managed to sustain their economies despite significant money printing, thanks to their governments' credibility.

Gold, once the backbone of monetary system, now lay dormant in vaults, its role as a medium of exchange obsolete.

In the past, money represented gold, deriving its credibility from this backing. Today, money has no connection to gold. Its value stems from government guarantees - as long as people trust the state, the money retains its worth.

Modern monetary issues are thus directly tied to government credibility rather than gold reserves. This shift allows governments considerable freedom in monetary policy. For instance, during the 2008 subprime crisis, the US implemented Quantitative Easing (QE), essentially printing large sums of money to prop up the economy.

While governments can print trillions at will, citizens struggle to earn even modest amounts. This disparity has led some to question government trustworthiness and seek alternative money - ones that hold intrinsic value without relying on government backing or gold reserves.

The search for a self-valuable money is underway...

The Era of Post-QE Money

What kind of money doesn't need government backing or gold reserves, yet remains credible on its own? What money can't be endlessly multiplied through Quantitative Easing?

What type of money possesses the qualities of being "scarce," "unforgeable," and "divisible into smaller units" like gold?

Bitcoin and Blockchain architecture provide (at least part of) the answer to these questions!

The dream of creating an alternative money owned and managed by the public, without a central intermediary, transparent, and with verifiable transactions, has become a reality. This concept was brought to life through Blockchain technology, invented by the mysterious scientist(s) using the pseudonym Satoshi Nakamoto in 2008.

While historical currencies were backed by gold reserves and modern currencies are guaranteed by (ostensibly trustworthy) governments, what backs Bitcoin and Blockchain?

Let's explore how Blockchain works and why it makes Bitcoin trustworthy without any external guarantees.

A Decentralized Central Banking System

Satoshi Nakamoto designed Bitcoin's architecture using Blockchain technology. Without delving into technical details, here's how Blockchain functions:

Initially, Bitcoin's Blockchain was programmed to have exactly 21 million Bitcoins in the system. Acquiring Bitcoin isn't simple and can be done in two ways:

- Mining Bitcoin (becoming a Bitcoin Miner)

- Purchasing Bitcoin from others at market price (currently about 35,000 Thai Baht per BTC)

Bitcoin miners are akin to gold miners. They invest in specialized equipment to mine Bitcoin from a complex system. As time passes, mining Bitcoin becomes increasingly difficult due to its limited supply.

The scarcity and effort required to obtain Bitcoin give it value, similar to gold. This is why Bitcoin doesn't need external backing - its value comes from its scarcity and limited supply.

Unlike central banks like the Federal Reserve that can print money at will, Bitcoin has no centralized authority. New Bitcoins enter the ecosystem randomly, and there's no way to produce more than the set 21 million limit. This fixed supply helps maintain Bitcoin's purchasing power, unlike traditional currencies subject to inflation through excessive printing.

To address concerns about hacking, let's consider an example:

Imagine I have 700,000 baht to exchange for 20 BTC through an agent. After the transaction, how can I be sure my 20 BTC will remain safe and not be hacked to zero?

The record of this 20 BTC transfer is stored as copies on "every computer" of millions of Bitcoin users worldwide. For someone to hack and steal my 20 BTC, they would need to alter this information on millions of computers globally simultaneously - a practically impossible task. This system is called a Distributed Ledger or Distributed Network.

Bitcoin's network essentially has millions of witnesses worldwide verifying every transaction. It's practically impossible for fraudsters to deceive all these witnesses simultaneously. As long as these witnesses exist, your funds remain secure (unless you lose your wallet’s seed key, which would be akin to losing your ATM card and PIN - a risk that exists with any currency).

This global distribution of Bitcoin's transaction data is the core of Blockchain technology, which has remained unhacked to this day.

Q: What about the reported hacks at Mt.Gox or Bitfinex?

A: The Blockchain system itself can't be hacked. When "Person A transfers 1 BTC to Person B," this transaction is irreversible and unalterable due to its worldwide replication and millions of global witnesses. The reported hacks at Mt.Gox and Bitfinex were actually cases of stolen keys, allowing unauthorized transfers. This type of data theft is a risk in any financial system, not unique to Bitcoin.

Summary

Bitcoin was created as a medium of exchange similar to gold: limited in quantity, scarce, unforgeable, and fraud-resistant. In essence, Bitcoin shares the same properties that made gold a universal medium of exchange for about 5,000 years of human history.

Bitcoin doesn't require a central banking system or government backing. As long as the internet exists, Bitcoin will continue to function. No government can effectively ban Bitcoin use unless they can restrict internet access entirely.

Bitcoin represents a decentralized, secure, and independent financial system that combines the historical reliability of gold with modern digital technology. Its design addresses many issues of traditional money while offering a new paradigm for global transactions.

As long as people maintain trust in Bitcoin, you'll always be able to exchange it for Thai baht or US dollars, much like trading gold. With Bitcoin in your possession, you can even purchase goods from certain merchants who accept it as payment.

Moreover, as people lose confidence in traditional currencies, they tend to seek assets that preserve their purchasing power, such as stocks, real estate, gold, and now Bitcoin.

Given this context, why wouldn't you trust Bitcoin if you're willing to trust dollars, yen, or euros? Central banks can manipulate these currencies through negative interest rates, quantitative easing, and taxation on transactions or even savings.

If people decide to use Bitcoin as a medium of exchange instead of traditional currencies, it means your Bitcoin holdings would be free from government and central bank control. You wouldn't need to worry about inflation due to money printing, tax increases, or negative interest rates affecting your bank deposits.

Recently, Japan has legalized Bitcoin as an alternative medium of exchange alongside the yen. The reasons behind this decision are worth exploring in detail.

These factors have contributed to Bitcoin's price surpassing $1,000. Long-term, Bitcoin will likely remain volatile and may experience significant drops. When that time comes, you'll need to decide whether to trust this new alternative currency or view it as just another economic bubble.

While this article may seem pro-Bitcoin, there are still several concerns about its usage that warrant discussion. Also, my cost basis for my Bitcoin holding is quite low, so I'm not encouraging purchases above $1,000. Bitcoin's price is purely based on people's confidence. It could potentially reach $10,000 or fall back to $100. If you're interested, make your own informed decision. In my portfolio, Bitcoin plays a role similar to gold – an alternative investment not exceeding 10-15% of the total. Before investing, it's advisable to read my another article about Bitcoin's potential drawbacks to get a balanced perspective.

The Dark Side of Bitcoin

Economic Challenges and Government Opposition | January 2017

Bitcoin is hailed as a new financial system that operates without a central authority like a central bank. This very lack of centralized control is what makes most governments wary of Bitcoin.

What do we really trust?

Our current financial system, known as fiat currency, relies on central banks to determine the money supply. Why do we trust in ink-stained paper with no tangible backing? The answer lies in our faith in state credit. When the government guarantees that this paper has value as a medium of exchange, we accept it.

Contrary to popular belief, governments haven't needed gold reserves to print money for a long time. This practice ended when President Richard Nixon abandoned the Bretton Woods System, decoupling dollars from gold.

This is why when a state collapses, its financial system follows suit, as seen in historical cases of hyperinflation in Zimbabwe or post-World War I Weimar Republic.

Why does the state need to control the money supply?

Central banks are the primary entities responsible for managing the money supply in an economy. In countries like Thailand, this might involve adding or removing money from the system by controlling interest rates. Major economies like the US, Japan, UK, and the Eurozone can even print money out of thin air.

These mechanisms, whether setting interest rates or quantitative easing (QE), are part of monetary policy - the central bank's toolkit for maintaining economic stability.

For example, during economic downturns, a state might choose to devalue its currency (through lowering interest rates or currency market interventions) to boost exports and ease economic pressures.

The Eurozone's single currency creates problems for weaker economies within it, as they can't use monetary policy to stimulate their economies independently. This has led to high debt levels and risk of bankruptcy for some member states.

In essence, appropriate central bank intervention is crucial for helping weak economies recover (Thailand's Tom Yum Kung crisis is a close-to-home example) or cooling overheating economies (as seen in China in recent years). However, it's worth noting that "hacking the game" through endless money creation, like the QE practices of major powers, is considered an unorthodox monetary policy that doesn't typically yield positive results.

This is why I believe a return to the Gold Standard is unlikely in our era. Pegging currency to gold removes the flexibility needed in monetary policy.

To be frank, monetary policies that control currency strength or weakness are essentially using economic mechanisms to interfere with natural laws like Charles Darwin's theory of Natural Selection. In simple terms, according to Darwin's principles, weaker countries would naturally struggle in economic warfare and eventually collapse.

If a country wants to improve its exports, it should focus on producing suitable goods, improving quality, or innovating to create competitive advantages, rather than devaluing its currency to make products cheaper.

Countries that can't adapt should, in theory, become extinct according to Darwinian principles.

Returning to Bitcoin...

Why are most governments concerned about Bitcoin?

This is because if citizens choose to use Bitcoin as a medium of exchange, the state will lose its ability to control the money supply through central bank mechanisms as it has done in the past. Consequently, economic problems could no longer be addressed through traditional monetary policy. The only tool left would be fiscal policy (such as government intervention through public spending).

In a world that uses Bitcoin, quantitative easing (QE) would no longer be possible. Without QE, many major powers would face bankruptcy. (During the Subprime crisis, the US would have gone bankrupt without QE, and the same applies to Japan and the Eurozone.)

If the entire world used Bitcoin, it would be similar to using gold. There would be no weak or strong currencies, no currency manipulation, and no Forex market for trading. We could use Bitcoin to buy ramen in Japan just as easily as we use it to buy boat noodles in Thailand.

Traditional banking systems might become obsolete when we have an independent financial system built on the internet.